If you’re a finance leader in a January through December fiscal year, December represents both your year-end close and your deadline for finalizing 2026 variable pay.

Waiting until March or April to release new plans is a pattern many teams fall into, and the consequences are predictable: frustrated reps, inconsistent accruals, and commission expenses that catch everyone by surprise.

As our VP of Go-to-Market, Ryan Milligan, put it during a recent webinar, “Businesses feel the pain of rolling out next year’s comp plans in March because reps are selling for months against a plan they don’t know.”

That uncertainty leads to turnover, demotivation, and messy handoffs between RevOps and Finance.

This guide breaks down four things Finance must lock in before the ball drops:

- Business goals

- ASC 340/606 implications

- Budgeting and headcount

- Automation readiness.

And at the end, we’ll link to a walkthrough showing how QuotaPath streamlines ASC 606 compliance for commission accounting.

Start with the Business, Not the Plan

Before touching formulas, rates, or accelerators, Finance should anchor 2026 variable pay to the company’s 2025–2026 goals. It sounds obvious, but it’s the most common gap between Sales and Finance.

Finance is responsible for cash stewardship and board expectations. Sales is responsible for motivation, clarity, and revenue.

Those motivations aren’t oppositional… but they need to be aligned early.

“Wouldn’t you hate to spend hours on a fantastic plan just to hear, ‘This doesn’t align at all with the company’s goals for the next year’?” said Amy Walker, CPA and Partner of Walker Glantz.

Start with a simple discovery conversation with RevOps and the CRO:

- What revenue and cash burn targets define success in 2026?

- Do we need to push multi-year or multi-product deals to improve NRR?

- Are we shifting the mix between new business and expansion?

- What buyer behaviors do we need to encourage or reduce?

Ryan advises approaching the CFO relationship like rep discovery: “You should interview your CFO the same way you’d interview a rep about their opinion of the comp plan.”

Doing this now prevents the late-stage rejection of an otherwise great plan.

Understand How ASC 340/606 Will Treat 2026 Variable Pay

Once the goals are clear, Finance should translate them into ASC 340/606 realities. This is where plan design and accounting collide.

ASC 340 often requires certain commissions, especially those tied to customer acquisition, to be capitalized and amortized over the customer’s anticipated life. ASC 606 then dictates when revenue is recognized, which impacts the timing of commission expense.

This is where many plans unintentionally get expensive. A simple switch, such as paying on the total contract value (TCV) instead of the annual contract value (ACV) or introducing a renewal commission, can meaningfully change amortization schedules.

“Those details are so important to iron out before the year even starts,” said Amy.

Finance should ensure the plan includes:

- Clear rules for when commissions are earned vs. paid

(e.g., payment begins when billing begins) - Treatment of multi-year contracts and delayed billing starts

- Rules for clawbacks, cancellations, and churn

- Distinction between commissions that must be capitalized vs. expensed immediately

Without this clarity, RevOps and Finance end up doing interpretive accounting every month… something no team wants in Q1.

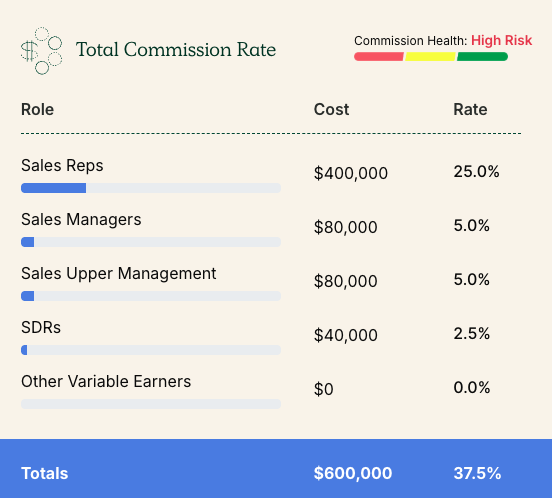

Total Commission Rate Calculator

Find the full cost of commissions per deal across roles with our free Total Commission Rate Calculator.

Use CalculatorBudget & Headcount: Can You Actually Afford This Plan?

With accounting rules in place, the next step is simple but essential: Can the business afford the 2026 plan?

Finance should start by evaluating the 2024 data:

- Total commissions paid

- Total new + expansion revenue

- Average effective commission rate

(total commissions ÷ revenue influenced)

This gives a baseline for what’s healthy, what’s trending upward, and what needs adjusting.

Next, layer scenario modeling for 2026:

- What happens at 80% attainment?

- At 100% attainment?

- At 120–130% attainment?

- What’s the cost impact of accelerators, multipliers, or SPIFs?

“You can hit your revenue target but overspend on commissions, and suddenly, finance is having an uncomfortable board conversation,” said Ryan.

From there, connect the model to headcount planning:

- Revenue target ÷ realistic quota per rep = required productive heads

- Adjust for average ramp (usually 3–6 months)

- Factor in expected attrition and time-to-fill

“My biggest fear was, did I miss something, and we’re going to not be able to afford this plan?” Amy said.

Modeling in December eliminates that fear and prevents mid-year resets that erode trust with reps.

Automation Readiness: Spreadsheets Won’t Survive 2026

Even when the plan is sound, spreadsheets can still break everything.

Manual commission processing often leads to:

- Formula mistakes

- No audit trail

- Version confusion

- Late closes

- Reps disputing payouts

- Inconsistent ASC 606 support

Amy shared an example of a client of theirs who relied on spreadsheets.

“Their sales reps were calculating their own commissions and turning them into payroll,” Amy said.

Under ASC 606/340, manual processes increase audit risk and make it nearly impossible to maintain amortization schedules accurately.

Finance should validate that for 2026, the business has:

- Centralized, documented plan logic

- Reliable CRM → revenue → commission mapping

- Automated calculations tied to deal data

- Exportable, audit-friendly reports

- Controls for approvals, changes, and historical adjustments

This is where tools like QuotaPath become a critical part of the finance tech stack. QuotaPath helps teams model new plans, automate calculations, enforce rules, and produce the exportable reports auditors expect, especially around ASC 606.

A Simple December Checklist for Finance

By December 31, Finance should be able to say “yes” to the following:

- We aligned with CRO/RevOps on 2026 revenue, cash, and behavioral goals.

- We understand ASC 340/606 implications of the 2026 plan and documented the accounting rules.

- We modeled total commission cost across low/target/high attainment scenarios.

- We validated headcount, ramp, and quota assumptions for 2026.

- We confirmed our commission system can support ASC 606 reporting and audits.

If not, there’s still time to fix it.

Design, track, and manage variable incentives with QuotaPath. Give your RevOps, finance, and sales teams transparency into sales compensation.

Talk to SalesWant to See How Your Plan Performs Under ASC 606?

QuotaPath can show you:

- How your 2024 commission structure would be amortized under ASC 606

- How 2026 plans will calculate automatically

- How to model winners/losers, total cost of commissions, and headcount impacts

- How Finance can get clean, repeatable exports for audits and month-end close